News & Updates

The latest news and updates from companies in the WLTH portfolio.

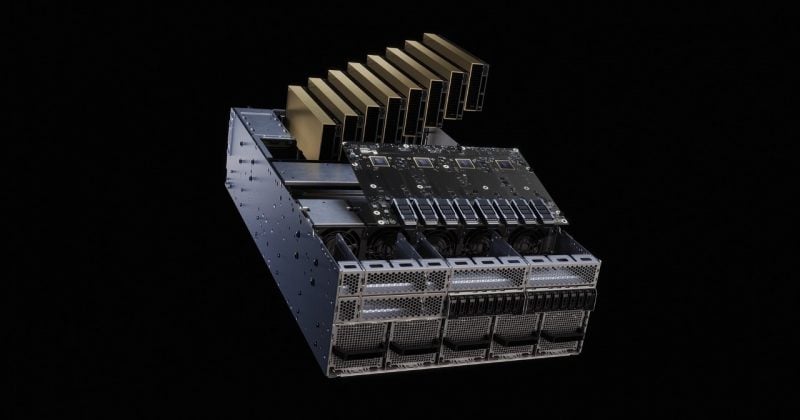

SpaceX $52B Nvidia server order claim lacks verification

A social media claim by @AndrewCurran_ suggests that SpaceX has ordered $52 billion worth of NVIDIA GB300-based AI servers from Foxconn. This unverified report appears to have sparked discussions around the potential impact on NVIDIA's market valuation. The claim, however, lacks confirmation from any official or verified sources and seems to conflate previous deals involving SpaceX, such as its known $6.3 billion computing agreement with Reflection AI and a $920 million per month GPU arrangement with Google. NVIDIA's GB300 systems are already recognized for their advanced AI capabilities, and Foxconn is confirmed as a major supplier of these systems, with shipments having begun in late 2025. Key Takeaways * The reported $52 billion order by SpaceX from Foxconn appears to have caught the attention of market participants, despite lacking verification. * NVIDIA's market prospects could be positively influenced by such demand, as indicated by current speculation. * The claim suggests heightened interest in NVIDIA's GB300 system capabilities, even though no official confirmation of the transaction exists. What to Watch Market participants are likely to monitor further announcements from NVIDIA or SpaceX that could confirm or refute this claim. Any official statements or financial disclosures will be crucial in assessing the credibility of the reported order. The ongoing activity could also be influenced by NVIDIA's upcoming quarterly earnings report, which may provide insights into their data center revenue and demand for AI systems. Get live prediction-market analysis, powered by Vera. Sign up for Vera.

SpaceX's blow-it-up testing won't fly on starship

SpaceX's willingness to blow stuff up and learn from the failures has propelled it from a cash-strapped startup to one of the world's most valuable companies (and kick-started a commercial space revolution along the way). The development of the Falcon 9 rocket was achieved over a relatively short period in space-industry time. That success was built on SpaceX's willingness to test, fail and repeat rapidly. The Falcon 1 rocket failed three times before reaching orbit on the fourth try in 2008 just before Chief Executive Officer Elon Musk's money ran out. SpaceX blew up a couple of rockets on the way to Falcon 9 reaching orbit, while Musk helped popularize the phrase "rapid unscheduled disassembly." This unique engineer-led culture is a reason that buy-side analysts have justified valuations for Musk's space venture that are, well, out of this world. SpaceX is adept at building complicated hardware and manufacturing almost all components in-house.

Foxconn Wins First SpaceX AI Server Contract Worth Estimated $52 Billion

Taiwan's Hon Hai Precision Industry, better known as Foxconn, has reportedly secured its first contract to manufacture artificial intelligence (AI) servers for Elon Musk's SpaceX, marking a major expansion of its AI infrastructure business. According to Taiwan's Economic Daily, the agreement could be worth about $52 billion, based on SpaceX's reported plan to deploy more than 13,000 AI server racks powered by Nvidia's next-generation GB300 chips. With each rack estimated to cost around $4 million, the deal would represent one of the largest AI server orders in the industry. The report said the contract would end the previous dominance of Dell Technologies and Super Micro Computer in supplying AI servers to SpaceX. It also strengthens Foxconn's position as a key manufacturing partner for major North American cloud computing and AI infrastructure companies. Foxconn has not commented on specific customer orders but has consistently highlighted strong demand for its AI server business. Chairman Liu Yangwei previously projected that the company would capture more than 40% of the global AI server market this year. He also expects AI rack shipments to double and continue growing through the end of 2026. Cloud and networking products, driven primarily by AI servers, have already become Foxconn's largest business segment. The Economic Daily reported that SpaceX recently increased its planned deployment of Nvidia GB300 server racks to approximately 13,000 units, with deliveries expected to begin in late 2026 and continue into the first quarter of 2027. Beyond its satellite and space launch operations, SpaceX is rapidly expanding its AI computing infrastructure. The report said the company has reached agreements involving Anthropic and Google while also advancing AI computing initiatives with the U.S. Department of Defense. These investments reflect SpaceX's broader push into cloud computing and artificial intelligence, creating new opportunities for suppliers such as Foxconn as demand for high-performance AI servers continues to accelerate.

SpaceX Targets Thursday Launch for Starship's 13th Test Flight After Last-Minute Delay

SpaceX (NASDAQ: SPCX) plans to launch the 13th test flight of its Starship rocket as early as Thursday, following the cancellation of a previous launch attempt just minutes before liftoff due to engine startup issues. The upcoming mission will focus on achieving a successful launch, ascent, stage separation, boostback burn, and landing burn at a designated offshore location. SpaceX also confirmed that the Starship vehicle will carry Starlink V3 satellites, marking another step in expanding its next-generation satellite internet network. The latest launch attempt was called off after several engines failed to ignite during the final countdown. The setback followed engine-related issues encountered during Starship's 12th test flight, which prompted an investigation by the Federal Aviation Administration (FAA). According to SpaceX, engineers have implemented multiple hardware and software upgrades to address the problems identified during the previous mission. The company said the changes are intended to improve the rocket's reliability and increase the likelihood of a successful test flight. The 13th Starship test will be the first since SpaceX completed its blockbuster initial public offering (IPO) in June. Investor sentiment has remained under pressure after last week's canceled launch, contributing to further declines in the company's share price. SpaceX stock has continued to trade below its IPO level, reflecting growing concerns over repeated testing delays and technical challenges. Since reaching a post-IPO peak market valuation of approximately $2.64 trillion, the company has lost roughly $1 trillion in market value. Despite the recent setbacks, Starship remains central to SpaceX's long-term ambitions, including deploying larger Starlink payloads, supporting future lunar missions, and eventually enabling human exploration of Mars. The upcoming test flight will be closely watched by investors, regulators, and the broader aerospace industry as the company seeks to demonstrate meaningful progress in its flagship rocket program.

SpaceX targets July 23 for next Starship launch after last-minute abort

Elon Musk's SpaceX is targeting July 23 for the 13th Starship test flight after a last-second launch abort last week. The mission will carry 20 Starlink satellites on a suborbital test as the company pushes toward routine orbital deployments by year-end. SpaceX is targeting Thursday, July 23, for another attempt to launch its Starship rocket, the company said in a statement on Sunday. SpaceX CEO Elon Musk posted on X later on Sunday that the next Starship launch would occur on Friday, contradicting the earlier statement from his company. He did not say whether the original Thursday date was wrong. On July 16, SpaceX's Starship rocket triggered a last-second abort before liftoff for its 13th flight test from Texas, which erased about $100 billion from the company's market value. SpaceX said it has modified Starship's propulsion system to address the engine issue experienced on the previous flight. A launch delay for the $15 billion rocket development program better known for dramatic engineering feats and explosive testing failures is not uncommon. On Friday, SpaceX said it would attempt the launch on July 20. The company has launched 12 Starship test flights since 2023. On its 13th flight test, Starship will carry 20 Starlink satellites to demonstrate its satellite-dispensing system and the Starlink network's laser communication links, but those satellites will follow the ship's suborbital trajectory and burn up in Earth's atmosphere soon after deployment. In its prospectus, SpaceX said that it aims to launch the first Starlink satellites to orbit on Starship by year's end, followed by routine launches.

Should You Buy $1,000 Worth of SpaceX Stock Before Its First Earnings Report?

One of the more recent arrivals to our stock market, Space Exploration Technologies (NASDAQ: SPCX), better known as SpaceX, has never published a quarterly earnings report as a publicly traded company. That's going to change soon. While the market doesn't yet have a firm date for when the figures for its second quarter ending June 30 might be released, it's reasonable to expect a report in early August. So there's time to consider if it's worth spending $1,000 on the company's stock. I wouldn't be willing, and here's why. Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue " Image source: Getty Images. Moving in the darkness One of the primary reasons is that SpaceX remains something of a mystery. Its name is somewhat misleading, since most of its operations aren't directly involved in space exploration. It has a thriving satellite business with Starlink, a high-capex artificial intelligence (AI) unit that builds data centers and manages the X (formerly Twitter) social media platform, as well as a space business. While the company intends for all these operations to complement each other, SpaceX is at present more of a jumble of activities that don't necessarily synthesize. That, plus the fact that the company's pre-IPO filings don't provide much detail about its finances, makes the second quarter hard to estimate. This is surely why analyst projections are all over the place. There are many pundits already tracking SpaceX stock; 25 of them are included in the data compiled by Yahoo! Finance, for example. But, unusually for analysts, their estimates don't sit within a relatively narrow range. Their figures for the quarter's revenue have a range of nearly $3 billion -- from $5.3 billion to $8.1 billion. Those prognosticators seem to agree that the historically loss-making SpaceX will also land in the red in the second quarter. The big question is by how much -- the current net loss estimates range from $0.12 to $0.42. Stuck on the launchpad Another element keeping me away from SpaceX is that it's still experiencing setbacks in its headline activity. Late Thursday afternoon, the company unexpectedly aborted the latest launch of its Starship rocket, after some of its engines apparently failed to start. Uncomfortably, this is the heavy rocket that's supposed to be the launch vehicle helping power the company to astronomical success and glory. Mission aborts happen, of course, but there's an awful lot of capital betting on that not to occur -- at least, not often -- at SpaceX. Understandably, the stock fell after the sudden cancellation (SpaceX stock fell 5% in Friday trading). With that decline, $1,000 would buy eight shares of SpaceX. That's not a huge commitment in the grand scheme of things, but even given that, I'd hold off on investing in this stock. The second quarter is sure to feature plenty of red ink, and the company still has at least one major operational kink to work out. I feel that money has better potential for liftoff in other stocks. Should you buy stock in Space Exploration Technologies right now? Before you buy stock in Space Exploration Technologies, consider this: The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now... and Space Exploration Technologies wasn't one of them. The 10 stocks that made the cut could produce monster returns in the coming years. Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you'd have $371,842!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you'd have $1,244,783!* Now, it's worth noting Stock Advisor's total average return is 900% -- a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors. See the 10 stocks " *Stock Advisor returns as of July 19, 2026. Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Kraken Fed Master Account Still Inactive Despite Historic Approval - TokenPost

Kraken's Wyoming-chartered bank made history in March by becoming the first crypto-focused institution to receive approval for a Federal Reserve master account. However, months after securing the milestone, the account has yet to become operational, highlighting the challenges of integrating crypto firms into the U.S. banking system. A Fed master account allows banks to hold funds directly with the Federal Reserve and transfer U.S. dollars through Fedwire without relying on intermediary banks. The Federal Reserve Bank of Kansas City approved Kraken's application on March 4 after the company had waited since October 2020. Despite the approval, Kraken Financial CEO David Mathena recently told Wyoming's blockchain select committee that the bank is still working to activate the account. The company is now focused on expanding its deposit services and preparing to fully utilize the direct Fed connection. Until then, Kraken continues to process U.S. dollar wire transfers through Dart Bank, according to its support documentation. Kraken has previously said the rollout would happen in phases, initially serving large institutional clients. The account also comes with unique restrictions. The Kansas City Fed approved it as a one-year pilot with undisclosed conditions tailored to the bank's risk profile. Those limitations have attracted scrutiny from lawmakers, including Representative Maxine Waters, who questioned the legal basis for the so-called "limited purpose account" and whether Kraken can access services such as ACH payments or earn interest on Fed balances. Kraken secured approval as a Tier 3 applicant, a category covering state-chartered banks without federal deposit insurance or a federal banking regulator. Such approvals are extremely rare. Federal Reserve Vice Chair for Supervision Michelle Bowman recently described Tier 3 access as nearly impossible to obtain. According to fintech analyst Jason Mikula, only three of 53 Tier 3 or unclassified applicants have ever received approval, with Kraken being the only crypto-related institution. The uncertainty continues as the Federal Reserve finalizes new rules governing payment account access for non-bank institutions. Public comments on the proposal close on July 27, while Governor Christopher Waller expects final regulations by the end of the year. Kraken's experience could influence the Fed's handling of future applications, including Ripple's pending request for a master account.

Should You Buy $1,000 Worth of SpaceX Stock Before Its First Earnings Report?

One of the more recent arrivals to our stock market, Space Exploration Technologies (NASDAQ: SPCX), better known as SpaceX, has never published a quarterly earnings report as a publicly traded company. That's going to change soon. While the market doesn't yet have a firm date for when the figures for its second quarter ending June 30 might be released, it's reasonable to expect a report in early August. So there's time to consider if it's worth spending $1,000 on the company's stock. I wouldn't be willing, and here's why. Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue " Moving in the darkness One of the primary reasons is that SpaceX remains something of a mystery. Its name is somewhat misleading, since most of its operations aren't directly involved in space exploration. It has a thriving satellite business with Starlink, a high-capex artificial intelligence (AI) unit that builds data centers and manages the X (formerly Twitter) social media platform, as well as a space business. While the company intends for all these operations to complement each other, SpaceX is at present more of a jumble of activities that don't necessarily synthesize. That, plus the fact that the company's pre-IPO filings don't provide much detail about its finances, makes the second quarter hard to estimate. This is surely why analyst projections are all over the place. There are many pundits already tracking SpaceX stock; 25 of them are included in the data compiled by Yahoo! Finance, for example. But, unusually for analysts, their estimates don't sit within a relatively narrow range. Their figures for the quarter's revenue have a range of nearly $3 billion -- from $5.3 billion to $8.1 billion. Those prognosticators seem to agree that the historically loss-making SpaceX will also land in the red in the second quarter. The big question is by how much -- the current net loss estimates range from $0.12 to $0.42. Stuck on the launchpad Another element keeping me away from SpaceX is that it's still experiencing setbacks in its headline activity. Late Thursday afternoon, the company unexpectedly aborted the latest launch of its Starship rocket, after some of its engines apparently failed to start. Uncomfortably, this is the heavy rocket that's supposed to be the launch vehicle helping power the company to astronomical success and glory.

SpaceX Starship Flight 13 Pushed to Friday July 24, 2026

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology. Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels. A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.

SpaceX moves Starship launch attempt to Thursday

July 19 (Reuters) - SpaceX is targeting Thursday, July 23, for another attempt to launch its Starship rocket, the company said in a statement on Sunday. SpaceX CEO Elon Musk posted on X later on Sunday that the next Starship launch would occur on Friday, contradicting the earlier statement from his company. He did not say whether the original Thursday date was wrong. On July 16, SpaceX's Starship rocket triggered a last-second abort before liftoff for its 13th flight test from Texas, which erased about $100 billion from the company's market value. SpaceX said it has modified Starship's propulsion system to address the engine issue experienced on the previous flight. A launch delay for the $15 billion rocket development program better known for dramatic engineering feats and explosive testing failures is not uncommon. On Friday, SpaceX said it would attempt the launch on July 20. The company has launched 12 Starship test flights since 2023. On its 13th flight test, Starship will carry 20 Starlink satellites to demonstrate its satellite-dispensing system and the Starlink network's laser communication links, but those satellites will follow the ship's suborbital trajectory and burn up in Earth's atmosphere soon after deployment. In its prospectus, SpaceX said that it aims to launch the first Starlink satellites to orbit on Starship by year's end, followed by routine launches. (Reporting by Gursimran Kaur in Bengaluru; Editing by Matthew Lewis)

Polymarket odds put Lula at 59.5% in Brazil race after 10-point jump

predict.info -- Premium Domain For Sale Domain only: USD 200,000. Prediction platform technology priced separately. predict.info Polymarket Reprices Brazil 2026 After Election-Legitimacy Headlines, Pushing Lula to 59.5% On Polymarket's Brazil Presidential Election market, Luiz Inácio Lula da Silva is priced at 59.5% after a sharp +10.0 percentage-point move, with $113,881,111 in volume. The repricing comes as a political-news cycle about election legitimacy resurfaced, giving traders a fresh catalyst to lean into (or fade) the front-runner premium. Key Takeaways * Polymarket's leading outcome is Luiz Inácio Lula da Silva at 59.5% (No 40.5%), ahead of Flávio Bolsonaro at 25.65% (No 74.35%). * The market widened the gap to the leader (+10.0 pp from 49.5% to 59.5%) as renewed public focus on election claims provided a sentiment catalyst. * This is a long-dated contract resolving on 2026-10-04, so near-term headlines can move price without providing settlement-level certainty. A new report describes differing public answers from Energy Secretary Chris Wright and DNI nominee Jay Clayton when asked whether Joe Biden won the 2020 U.S. election, after a televised address by President Donald Trump revived claims about interference and integrity. The piece says multiple audits, court rulings, and independent reviews upheld Biden's victory, while some Republicans publicly rejected Trump's renewed allegations. It also notes Senate Intelligence Committee Democrats criticized Clayton's refusal to directly state that Biden won, and Senator Mark Warner said the exchange is why he would oppose Clayton's nomination. Odds & Liquidity Check: Lula +10.0pp to 59.5% on $113,881,111 Volume; Flávio Bolsonaro at 25.65% This Polymarket contract is a multi-outcome election market: each candidate has their own Yes/No price, and exactly one outcome resolves as the winner at settlement rather than "the market" settling at a single number. At snapshot time, Lula's line sits at Yes 59.5% / No 40.5%, while the main challenger Flávio Bolsonaro is Yes 25.65% / No 74.35% -- a spread that implies traders see the race as meaningfully tilted but not locked. The latest move is a fast +10.0 pp jump in the leader from 49.5% to 59.5% on $113,881,111 volume, a sign the market is willing to pay up for the front-runner even as the historical summary flags moderate volatility and a "weakening" consensus (latest odds in the summary: 49.5%, with -11.0 pp over both 24h and 7d). That combination -- big spot repricing alongside a negative short-window change in the summary -- signals two-way disagreement: traders are still actively testing levels rather than converging on a stable probability. Compared with slower narrative formation in traditional political coverage, this market's continuously traded prices show where traders are willing to take risk right now, but the 2026-10-04 resolution date means the contract will remain highly sensitive to non-settlement headlines for a long time. Watch whether the leader's premium holds above the ~60% area while the market is still labeling consensus as weakening; sustained holding would suggest traders are converting headline catalysts into a more durable baseline. Also monitor whether the second-place contract (Flávio Bolsonaro) compresses from 25.65% or stays wide -- multi-outcome markets often show meaningful information in how quickly the runner-up rebounds (or fails to) after a leader spike. Cross-Market Watchlist on Polymarket: U.S. Election-Legitimacy Contracts and Other Macro/Crypto Event Markets Traders Tr If you're building a cross-market watchlist on Polymarket, it's worth keeping an eye on adjacent contracts where traders are also repricing long-horizon political risk. The biggest tape right now is 19.75% on "Democratic Presidential Nominee 2028" (leading outcome: Gavin Newsom) on $1,242,441,083 in volume, alongside 34.8% on "Next French Presidential Election" (leading outcome: Marine Le Pen) with $114,963,312 traded. Watching how these odds move in parallel can help contextualize whether flows are idiosyncratic to one race or part of a broader risk-on/risk-off shift across the platform. Odds Trend By the Numbers * Platform: Polymarket * Market: Brazil Presidential Election * Contract type: Price strike ladder: each rung has separate Yes/No; Yes means the spot price is above that USD strike at settlement. * Resolution window: Oct 04, 2026 (UTC) * Status: Active (open for trading) * Volume: ~$113,881,111 Top strike rungs +13 more strikes not shown

Polymarket odds for Hormuz traffic normalizing by year-end slide to 52.5%

Polymarket Reprices Strait of Hormuz "Traffic Normalizes by Dec. 31" After Ninth Night of U.S. Strikes On Polymarket, the contract "Strait of Hormuz traffic returns to normal by December 31?" is priced at 52.5% Yes on $5.40M matched volume, after a sharp repricing from 85.5%. The move follows a fresh headline about U.S. forces striking Iran for a ninth consecutive night, and the market's shift is visible directly in the implied probability. Key Takeaways * Polymarket currently implies a 52.5% chance (Yes) that Strait of Hormuz traffic returns to normal by Dec. 31. * Traders repriced the contract lower after a new headline about continued U.S. strikes, pushing odds down from 85.5% to 52.5%. * Settlement is tied to conditions by 2026-12-31; near-term tape shows moderate volatility with -2.0 pp over both 24h and 7d. A brief headline reports that U.S. forces struck Iran for the ninth consecutive night, citing Central Command. The update adds to ongoing conflict-related uncertainty that traders may connect to regional shipping risk and timelines. Odds Collapse From 85.5% to 52.5% Yes on $5.40M Matched Volume -- Coin-Flip Pricing Near 50% At 52.5% Yes vs 47.5% No, Polymarket is now close to a coin-flip on whether traffic normalizes by year-end -- down 33.0 percentage points from the prior 85.5% reference, a large confidence reset rather than a marginal drift. With $5,403,416 matched, this isn't a thin-market blip; the price is reflecting meaningful two-sided disagreement about the timeline. The contract is a simple binary: buying Yes pays out if the "returns to normal by December 31" condition is met by the 2026-12-31 resolution date; buying No pays out otherwise, so the entire debate is being expressed as a single probability rather than a narrative. Even while the broader summary flags bearish trend, moderate momentum, and reversal_detected=true, the shorter-window stats show only -2.0 pp over both 24h and 7d -- suggesting the big repricing is the dominant signal, while the latest tape has been comparatively stable around its new range. Watch whether the market can hold above the 50% line: a sustained move back toward the mid-80s would indicate traders re-embracing a fast-normalization timeline, while continued sub-50% pricing would imply the year-end deadline is being treated as more likely to be missed as the contract approaches 2026-12-31. Cross-Contract Watchlist: How Traders Hedge Shipping-Risk Bets With Macro and Crypto Polymarket Markets Zooming out from the core shipping-risk line, traders often hedge timeline uncertainty by scanning adjacent Polymarket contracts that price nearer-term normalization, ceasefire durability, and broader escalation risk. The tightest near-date read is 98.35% No on $18,408,562 matched for "Strait of Hormuz traffic returns to normal by July 31?", while conflict-duration framing shows 99.1% on $655,123 for "Israel x Iran ceasefire continues through...?". On the tail-risk side, "Will the U.S. invade Iran before 2027?" sits at 69.5% No on $44,953,022, and leadership-path pricing appears in "Iran leader end of 2026?" at 73.3% on $32,658,882 -- useful cross-checks for how the platform is distributing risk across horizons. Odds Trend By the Numbers * Platform: Polymarket * Market: Strait of Hormuz traffic returns to normal by December 31? * Resolution window: Dec 31, 2026 (UTC) * Status: Active (open for trading) * Leading implied prob.: 52.5% * Volume: ~$5,403,416 * Top outcomes: Yes: Yes 52.5% / No 47.5%; No: Yes 52.5% / No 47.5%

SpaceX moves Starship launch attempt to Thursday

July 19 (Reuters) - SpaceX is targeting Thursday, July 23, for another attempt to launch its Starship rocket, the company said in a statement on Sunday. SpaceX CEO Elon Musk posted on X later on Sunday that the next Starship launch would occur on Friday, contradicting the earlier statement from his company. He did not say whether the original Thursday date was wrong. On July 16, SpaceX's Starship rocket triggered a last-second abort before liftoff for its 13th flight test from Texas, which erased about $100 billion from the company's market value. SpaceX said it has modified Starship's propulsion system to address the engine issue experienced on the previous flight. A launch delay for the $15 billion rocket development program better known for dramatic engineering feats and explosive testing failures is not uncommon. On Friday, SpaceX said it would attempt the launch on July 20. The company has launched 12 Starship test flights since 2023. On its 13th flight test, Starship will carry 20 Starlink satellites to demonstrate its satellite-dispensing system and the Starlink network's laser communication links, but those satellites will follow the ship's suborbital trajectory and burn up in Earth's atmosphere soon after deployment. In its prospectus, SpaceX said that it aims to launch the first Starlink satellites to orbit on Starship by year's end, followed by routine launches. (Reporting by Gursimran Kaur in Bengaluru; Editing by Matthew Lewis)

Even With Elon Musk's SpaceX Stock (SPCX) Down Below Its IPO Price, I'd Still Rather Buy This Dividend Stock in July

There's been a lot of attention paid to Elon Musk's company Space Exploration Technologies (NASDAQ: SPCX), or SpaceX, and excitement over its debut on the stock market in June via an initial public offering (IPO). It was a huge IPO, raising some $75 billion and seeing the stock surge 19% to $193 on its first day. But the stock has struggled since and was recently below its IPO price, trading near $126 on July 17. Should you invest in SpaceX now? Well, you could. But I think there's a better stock to buy. Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks " Image source: Getty Images. Consider General Mills Food giant General Mills (NYSE: GIS) is close to the opposite of SPX Technologies. Founded 160 years ago, in 1866, it's grown to be a powerhouse in the food sector, with brands such as Annie's, Betty Crocker, Bisquick, Cascadian Farm, Cheerios, Chex, Cinnamon Toast Crunch, Gold Medal, Green Giant, Kix, Larabar, Nature Valley, Old El Paso, Progresso, Totino's, Wanchai Ferry, and Wheaties -- among many others. Why invest in this specialist in cereals and much more? Well, several reasons: First, it's a solid dividend-paying stock, with a boffo recent dividend yield of 6.3%. Better still, the company has also been repurchasing shares (which rewards shareholders by making remaining shares more valuable), sending its total shareholder yield up to a recent 8.7%. (General Mills has paid a dividend for 127 consecutive years.) The stock is also looking undervalued, with a recent forward-looking price-to-earnings (P/E) ratio of 12.5, well below the five-year average of 15, and a price-to-sales ratio of 1.1, well below the five-year average of 1.8. The stock is appealingly priced, largely because it has fallen lately -- averaging annual losses of 15% over the past three years. In its third-quarter report, management pointed to several issues that affected its third quarter: retailer inventories and weather-related supply chain disruptions, along with brand-improving investments, divestitures, and unfavorable trade expense timing, among others. It noted, though, that these "timing headwinds [are] expected to become tailwinds in Q4." In the fourth quarter, CEO Jeff Harmening pointed to a continuing turnaround: We are laser focused on increasing our efficiency to help offset elevated inflation, fund our growth investments, and generate stronger earnings and cash flow. ... We're targeting $3 billion in cumulative cost savings by fiscal 2030. ... I'm confident we're on the path to restoring profitable growth and driving shareholder value over the long term. Recession resistance Here's a last reason to consider General Mills: Many are worrying about a stock market crash coming this year or soon, potentially with a recession following. If that does happen, it's often high-flying growth stocks that will fall most sharply. The companies that tend to hold their value relatively well are defensive ones -- those selling things that everyone needs. In a recession, you might put off getting a new car or dishwasher, but you'll still pay for electricity and your medications, as well as your Cheerios and Green Giant veggies. Given all that, I'd much rather invest in General Mills than SpaceX. Should you buy stock in General Mills right now? Before you buy stock in General Mills, consider this: The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now... and General Mills wasn't one of them. The 10 stocks that made the cut could produce monster returns in the coming years. Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you'd have $371,842!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you'd have $1,244,783!* Now, it's worth noting Stock Advisor's total average return is 900% -- a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors. See the 10 stocks " *Stock Advisor returns as of July 19, 2026. Selena Maranjian has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Should You Buy $1,000 Worth of SpaceX Stock Before Its First Earnings Report?

One of the more recent arrivals to our stock market, Space Exploration Technologies (SPCX 5.41%), better known as SpaceX, has never published a quarterly earnings report as a publicly traded company. That's going to change soon. While the market doesn't yet have a firm date for when the figures for its second quarter ending June 30 might be released, it's reasonable to expect a report in early August. So there's time to consider if it's worth spending $1,000 on the company's stock. I wouldn't be willing, and here's why. Moving in the darkness One of the primary reasons is that SpaceX remains something of a mystery. Its name is somewhat misleading, since most of its operations aren't directly involved in space exploration. It has a thriving satellite business with Starlink, a high-capex artificial intelligence (AI) unit that builds data centers and manages the X (formerly Twitter) social media platform, as well as a space business. While the company intends for all these operations to complement each other, SpaceX is at present more of a jumble of activities that don't necessarily synthesize. That, plus the fact that the company's pre-IPO filings don't provide much detail about its finances, makes the second quarter hard to estimate. This is surely why analyst projections are all over the place. There are many pundits already tracking SpaceX stock; 25 of them are included in the data compiled by Yahoo! Finance, for example. But, unusually for analysts, their estimates don't sit within a relatively narrow range. Their figures for the quarter's revenue have a range of nearly $3 billion -- from $5.3 billion to $8.1 billion. Those prognosticators seem to agree that the historically loss-making SpaceX will also land in the red in the second quarter. The big question is by how much -- the current net loss estimates range from $0.12 to $0.42. Stuck on the launchpad Another element keeping me away from SpaceX is that it's still experiencing setbacks in its headline activity. Late Thursday afternoon, the company unexpectedly aborted the latest launch of its Starship rocket, after some of its engines apparently failed to start. Uncomfortably, this is the heavy rocket that's supposed to be the launch vehicle helping power the company to astronomical success and glory. Mission aborts happen, of course, but there's an awful lot of capital betting on that not to occur -- at least, not often -- at SpaceX. Understandably, the stock fell after the sudden cancellation (SpaceX stock fell 5% in Friday trading). With that decline, $1,000 would buy eight shares of SpaceX. That's not a huge commitment in the grand scheme of things, but even given that, I'd hold off on investing in this stock. The second quarter is sure to feature plenty of red ink, and the company still has at least one major operational kink to work out. I feel that money has better potential for liftoff in other stocks.

SpaceX Moves Starship Launch Attempt to Thursday

SpaceX is targeting Thursday, July 23, for another attempt to launch its Starship rocket, the company said in a statement on Sunday. SpaceX CEO Elon Musk posted on X later on Sunday that the next Starship launch would occur on Friday, contradicting the earlier statement from his company. He did not say whether the original Thursday date was wrong. On July 16, SpaceX's Starship rocket triggered a last-second abort before liftoff for its 13th flight test from Texas, which erased about $100 billion from the company's market value. SpaceX said it has modified Starship's propulsion system to address the engine issue experienced on the previous flight. A launch delay for the $15 billion rocket development program better known for dramatic engineering feats and explosive testing failures is not uncommon. On Friday, SpaceX said it would attempt the launch on July 20. The company has launched 12 Starship test flights since 2023. On its 13th flight test, Starship will carry 20 Starlink satellites to demonstrate its satellite-dispensing system and the Starlink network's laser communication links, but those satellites will follow the ship's suborbital trajectory and burn up in Earth's atmosphere soon after deployment. In its prospectus, SpaceX said that it aims to launch the first Starlink satellites to orbit on Starship by year's end, followed by routine launches.

Beyond the coffee fix: Unconventional, science-backed strategies to recover from a sleepless night - NaturalNews.com

* Pharm.D. Zeke Medina advises using proteins and healthy fats, like nuts and whole wheat, to stabilize blood sugar after poor sleep. * Neuroscientist Major Allison Brager emphasizes that early morning light exposure is crucial for resetting the sleep system and promoting alertness. * The circadian rhythm is a 24-hour internal clock that prepares the body for regular transitions like sleep and wakefulness. * Medina warns against going to bed excessively early to "catch up," stating that consistency in wake-up times anchors your rhythm. * A short power nap may help, but experts caution that longer or irregular naps can disrupt nighttime sleep. While experts agree that consistent, quality sleep is non-negotiable for health, the reality of an occasional restless night is universal. The standard advice, have some coffee, power through, only scratches the surface. A deeper dive into sleep science and long-standing wellness principles reveals a more nuanced playbook for recovery, one that involves strategic nutrition, light exposure and a strict commitment to rhythm. After a poor night's sleep, the body's energy systems are depleted. The craving for quick sugar is a trap, leading to an insulin spike and subsequent crash. While coffee's caffeine can temporarily block sleep-inducing adenosine, sustainable energy must come from elsewhere. "My favorites are mixed nuts, veggies with hummus or anything with whole wheat and nut butter," advises Pharm.D. Zeke Medina, emphasizing proteins and healthy fats to stabilize blood sugar. This aligns with broader nutritional wisdom that cautions against evening intake of fatty foods, sugar and white flour, all of which can disrupt sleep onset. The goal the next day is to avoid these same energy-sabotaging foods, opting instead for steady fuel. Harnessing light and rhythm Perhaps the most potent tool is light. Neuroscientist Major Allison Brager, Ph.D., notes our sleep system "resets" through early morning light exposure. Getting sun, even through a window, signals the body to promote alertness. This complements the fundamental practice of obtaining enough exercise outdoors during the day, which reinforces natural circadian cycles. As noted by BrightU.AI's Enoch, the circadian rhythm is a 24-hour internal clock that governs our daily physiological patterns, enabling the body to adapt to transitions like sleep and wakefulness. These natural cycles prepare us for regular environmental changes, such as from day to night. The cornerstone of recovery, however, is resisting the urge to overcorrect. "Your circadian rhythm is anchored by your original bed and wake time," Medina explains. Going to bed excessively early to "catch up" can backfire. Consistency is vital; the body thrives on regular rhythmic cycles. This means waking at your usual time, even after a bad night and avoiding the disruptive temptation to sleep in on weekends. The nap paradox and active recovery The role of napping is personal and precise. A short "power nap" of 5-30 minutes may improve alertness and emotional regulation. However, experts warn it can perpetuate poor nighttime sleep if not managed. For some, daytime naps make nocturnal sleep more difficult. The key is consistency and brevity: If you nap, do so regularly and keep it under an hour. When fatigue hits, movement trumps stagnation. A moderate walk promotes wakefulness and increases blood flow without being overly strenuous. This echoes the recommendation for regular afternoon or evening exercise (though not right before bed) and a quiet 30-45 minute walk in fresh air before bedtime as a sleep-promoting ritual. Building better sleep for tomorrow Today's recovery is linked to tonight's sleep. Experts universally warn against sleep disruptors: caffeine after lunch, alcohol, nicotine and heavy evening meals. Instead, they promote sleep-supportive habits: a cool room (60-65°F) with fresh air circulation, a hot bath 1-2 hours before bed and a focus on calming foods. Foods containing the amino acid tryptophan, like figs, dates and whole grain crackers, can promote sleep. At the same time, items high in tyramine (like aged cheese, processed meats and tomatoes) should be avoided in the evening as they stimulate the brain. Ultimately, the path to recovering from and preventing sleepless nights is holistic. It intertwines disciplined daily habits, mindful nutrition and an understanding of the body's innate rhythms. As one timeless piece of advice succinctly puts it: "Regularity in your habits is important. This is vital to good sleep." The journey to better days starts not just with a morning coffee, but with a commitment to respecting the intricate science of sleep itself. Watch this video explaining why sleep deprivation is deadly. This video is from the High Hopes channel on Brighteon.com.

Is Polymarket down? Is polymarket down right now

If you're trying to beat the odds, bad luck. Polymarket is having some problems Saturday. According to DownDetector, Polymarket, a decentralized prediction market that allows users to bet on the outcome of real-world events using cryptocurrency, has been giving users some issues Saturday. The problems started around 8:30 p.m. EST and there were about 500 reports as of 8:45 p.m.. According to Downdetector, about 70 percent of the complaints were about the app, though betting and the website were also giving users some problems. It was also a topic on social media and "Is Polymarket down" was trending on Google. There is no timetable for when the issues will be resolved, though it hasn't been down long, so it could be a quick fix. This article originally appeared on Asbury Park Press: Is Polymarket down? Is polymarket down right now

Polymarket odds for Putin exit by June 2027 jump to 19% on $17.8M

predict.info -- Premium Domain For Sale Domain only: USD 200,000. Prediction platform technology priced separately. predict.info Drone-Attack Fire Reports Trigger Polymarket Repricing in "Putin Out by June 30, 2027" Ladder Polymarket's ladder market on whether Vladimir Putin is out as President of Russia by June 30, 2027 is priced at 19% Yes (81% No) on $17.83M volume, up 10.5 percentage points from 8.5%. The move follows reports of a drone attack and fires at fuel and logistics sites in Moscow region, offering a clear read on how traders are mapping near-term security shocks onto longer-dated leadership risk. Key Takeaways * Polymarket implies a 19% chance Putin is out as President of Russia by June 30, 2027 (81% No). * After drone-attack fire reports in Moscow region, traders pushed the June 30, 2027 strike higher, signaling more weight on leadership-disruption tail risk than before. * Settlement is pegged to the June 30, 2027 deadline; the market has been volatile lately with the latest odds (8.5%) below the recent average (16.6%). A report described a nighttime drone attack in Russia's Moscow region that sparked fires at an oil depot in Noginsk and at a Wildberries logistics center in Elektrostal, with videos showing explosions and large fires. The regional governor was cited as confirming drones struck the Noginsk depot and saying nearly 50 drones targeted the region overnight. Odds Curve & Liquidity Snapshot: June 30, 2027 Jumps to 19% Yes on $17.83M Volume (+10.5 pp) vs Dec 31, 2026 at 9% This is a price-ladder contract: each dated strike is a separate Yes/No market on whether Putin is out by that deadline, not a single "final date" settlement price. The curve shows traders assigning low near-term probability but a materially higher longer-horizon tail: December 31, 2026 sits at 9% Yes / 91% No, while June 30, 2027 is 19% Yes / 81% No; the earlier rungs are thinner odds at September 30, 2026 (4.1% Yes / 95.9% No) and July 31, 2026 (0.4% Yes / 99.6% No). The headline move is the June 30, 2027 strike jumping to 19% from 8.5% (+10.5 pp) with $17.83M traded, indicating meaningful disagreement being repriced into the farthest deadline rather than concentrated on the immediate rungs. At the same time, the provided summary flags a bearish, strong-momentum tape with latest odds at 8.5% versus a 16.6 average over the last five observations and -5 pp over both 24h and 7d, which is consistent with fast mean-reversion and sensitivity to short-lived catalysts rather than a steady drift upward. Watch whether buying pressure lifts the mid-curve (December 31, 2026 at 9% Yes) alongside the far strike (June 30, 2027 at 19% Yes); a curve that steepens only at the far end usually means traders see risk as long-dated and hard to time. Also monitor whether the market's recent bearish momentum (latest below recent average) persists or snaps back, which would signal the repricing was more than a one-off reaction. Cross-Contract Watchlist: How This Leadership-Risk Reprice Can Spill Into Polymarket Macro and Crypto Volatility Markets If you're tracking how a leadership-risk reprice can cascade across the tape, it's worth scanning what else traders are leaning into on Polymarket right now. In politics-adjacent flow, "Will the U.S. invade Iran before 2027?" sits at 68.5% No on $44.64M volume, while "Next leader out of power before 2027? (No Orban)" has "Starmer - UK PM" at 99.4% on a hefty $66.87M traded -- both useful for gauging broader risk appetite and time-horizon positioning. And away from macro entirely, even evergreen event markets like "World Cup: Golden Ball Winner" show how concentrated conviction can get, with "Lionel Messi" leading at 90.6% on $12.52M volume. Odds Trend By the Numbers * Platform: Polymarket * Market: Putin out as President of Russia by...? * Contract type: Price strike ladder: each rung has separate Yes/No; Yes means the spot price is above that USD strike at settlement. * Resolution window: Jun 30, 2027 (UTC) * Status: Active (open for trading) * Volume: ~$17,827,866 Top strike rungs +1 more strikes not shown

Polymarket prices Starmer exit-before-2027 at 99.4% on $66.9M volume

predict.info -- Premium Domain For Sale Domain only: USD 200,000. Prediction platform technology priced separately. predict.info Polymarket Pins "Starmer - UK PM" Near 99% as Election-Headline Risk Reprices the "Next Leader Out Before 2027" Contract Polymarket's "Next leader out of power before 2027? (No Orban)" market is priced as a near-lock for "Starmer - UK PM," with the leading outcome at 99.4% on $66.9M in volume. The move comes as election-news coverage continues to feed headline risk into how traders rank the next leader to fall, and the contract's recent odds ramp shows how quickly the market consolidated around one pick. Key Takeaways * Prediction: "Starmer - UK PM" leads at 99.4% implied probability in Polymarket's multi-outcome market. * Basis: Traders have concentrated almost entirely into the Starmer outcome, nudging it up +0.3pp (99.1% to 99.4%) alongside heavy total volume ($66.9M). * Timing: The market resolves by 2026-12-31, with a sharp +29.6pp move over both the last 24h and 7d in the available summary. A rolling elections news roundup circulated fresh political headlines across multiple jurisdictions, keeping attention on leadership stability and turnover narratives. That general stream of updates is the near-term catalyst traders often map onto "who exits first" markets, even when the information is diffuse rather than a single decisive event. Market Reaction: $66.9M Volume, 99.4% Implied Odds, and a +29.6pp Weekly Consolidation Into the Leading Outcome This is a multi-outcome Polymarket contract: you are not buying a generic "Yes/No" on one leader, you are picking which named leader is the next to be out of power before 2027, with settlement determined by which outcome is correct by the resolution date. Pricing is extremely one-sided: "Starmer - UK PM" sits at 99.4% Yes / 0.6% No, while long-shot alternatives such as "Trump - USA President" are 0.15% Yes / 99.85% No and "Putin - Russia President" is 0.25% Yes / 99.75% No -- showing the market is treating almost every other path as de minimis. The latest tick was a small +0.3pp lift (99.1% to 99.4%), but the historical summary signals a much bigger consolidation recently: +29.6pp over both 24 hours and 7 days, with a bullish trend, moderate momentum, moderate volatility, and "strengthening" consensus. With $66.9M in volume, the key informational takeaway is not a day-to-day micro move but that traders have largely converged on one resolution narrative rather than expressing sustained disagreement across outcomes. Watch whether the leading outcome stays pinned near 99% or drifts lower as attention rotates across leaders; any meaningful shift would likely show up first as small but persistent re-pricing into the sub-1% outcomes rather than a single abrupt flip, given how concentrated the market already is ahead of the 2026-12-31 resolution. Cross-Contract Watchlist: How This "Leader Out Before 2027" Trade Compares to Other Polymarket Leadership-Turnover and M Zooming out from this one leadership-turnover slate, Polymarket traders are also rotating into bigger-cycle political pricing where liquidity and narrative risk can look very different. "Presidential Election Winner 2028" has JD Vance leading at 19.75% on $663,674,366 in volume (+3.35pp), while "Republican Presidential Nominee 2028" prices Robert F. Kennedy Jr. at 49.0% on $676,486,070. For a nearer-term, binary-style read on executive stability, "Trump out as President by July 31?" sits at 99.55% for No on $1,476,092 (+0.4pp), offering a contrast between long-horizon field markets and tight-deadline yes/no contracts. Odds Trend By the Numbers * Platform: Polymarket * Market: Next leader out of power before 2027? (No Orban) * Contract type: Price strike ladder: each rung has separate Yes/No; Yes means the spot price is above that USD strike at settlement. * Resolution window: Dec 31, 2026 (UTC) * Status: Active (open for trading) * Volume: ~$66,870,814 Top strike rungs +20 more strikes not shown