News & Updates

The latest news and updates from companies in the WLTH portfolio.

Intel joins Musk's Terafab project to build a massive AI chip system with Tesla, SpaceX, and xAI - The Tech Portal

Intel has joined Elon Musk's Terafab initiative, teaming up with Tesla, SpaceX, and xAI to build a tightly integrated, next-generation chip manufacturing ecosystem. The project aims to centralize everything from chip design to fabrication and packaging, and is designed to produce AI processors at an unprecedented scale - targeting up to a terawatt of compute capacity annually. Intel's role will focus on providing advanced chip manufacturing expertise, positioning it as a key manufacturing partner in powering Musk's expanding AI and robotics ambitions. "Our ability to design, fabricate, and package ultra-high-performance chips at scale will help accelerate Terafab's aim to produce 1 TW/year of compute to power future advances in AI and robotics," the semiconductor giant said. Notably, Terafab aims to transform how semiconductor chips are produced by bringing design, manufacturing, packaging, and testing into a single integrated facility, instead of relying on a global network spread across the United States, Taiwan, and South Korea. The move comes at a time when demand for AI computing power is rising sharply, driven by technologies like generative AI, large language models, and autonomous systems. Currently, companies like Nvidia dominate AI chip design, while manufacturers like TSMC play a central role in production. Therefore, Terafab is positioned as an effort to challenge this model by creating a high-capacity, end-to-end system capable of producing advanced AI chips more efficiently and at scale. Financially, early estimates suggest an initial investment in the range of $20-25 billion, with the potential for significantly higher capital requirements as the project expands. And now, Intel's participation is seen as a crucial boost to the project, given its deep expertise in chip manufacturing and its push to regain leadership in advanced technologies. The company has been investing in next-generation processes like 18A and advanced packaging methods that combine multiple chip components into high-performance units. By partnering with Musk's ecosystem, Intel not only secures strong demand from companies like Tesla and xAI but also strengthens its position in the fast-growing AI hardware market, which is expected to reach hundreds of billions of dollars in the coming years. For Musk's companies, the latest deal helps connect hardware and AI more tightly. Tesla is already building custom chips for self-driving and robots like Optimus, while xAI is developing large AI models that need huge computing power. SpaceX adds to the plan with ideas for space-based data centers using solar energy and natural cooling. Together, this increases demand for highly efficient, specialized chips that Terafab aims to produce at scale. However, the development comes at a crucial time for Intel, which has been under financial pressure despite strong industry backing. Last year, Nvidia invested about $5 billion in Intel, taking over a 4% stake, while the US government also acquired a 10% stake through an $8.9 billion investment under federal chip programs. Despite this support, Intel reported a 4% drop in revenue to around $13.7 billion and a net loss of about $591 million in Q4 FY2025. The Tech Portal is published by Blue Box Media Private Limited. Our investors have no influence over our reporting. Read our full Ownership and Funding Disclosure →

Broadcom stock rises on Google, Anthropic deals

Broadcom (AVGO) stock gained in early trading on Tuesday, after the company announced two separate deals for its custom AI processors on Monday, one with Google (GOOG, GOOGL) and the other with Google and Anthropic (ANTH.PVT). The stock of the chipmaker rose more than 3% on the news, while the rest of the market largely declined due to President Trump's latest Iran threats. According to Broadcom's 8-K, the company has entered into a long-term agreement to develop and supply future custom Tensor Processing Units (TPUs) to Google, as well as a supply assurance agreement under which Google will use Broadcom's networking components in its next-generation AI server racks through 2031. The companies didn't disclose the financial terms of the agreements. Broadcom also said it is expanding its current agreement with Google and Anthropic that will allow Anthropic to access 3.5 gigawatts of Google's next-generation TPUs. That agreement is dependent on Anthropic's continued commercial success. But that doesn't appear to be an issue for Anthropic at the moment. In a press release announcing the news, Anthropic noted that its revenue run-rate has surpassed $30 billion, up from $9 billion at the end of 2025 thanks to demand for the company's Claude platform. The number of businesses spending more than $1 million annually with Anthropic has also grown from 500 companies in February to 1,000 as of April 6. BofA Global Research analyst Vivek Arya wrote in a note to investors on Monday that the moves provide greater visibility into Broadcom's plans moving forward and, "remove some prior stock overhang" on fears that Google would insource some of its manufacturing through customer owned tooling or use other manufacturers like MediaTek. Customer owned tooling (CoT) provides companies with greater oversight of the chip manufacturing process, but carries greater risk than fully outsourcing to a firm like Broadcom. "We believe [Broadcom] is well-positioned to gain accelerator share in CY26 and CY27 (from <10% in CY25 toward ~15%+), now backed by further expansions with Google and Anthropic (on top of prior OpenAI 1-10 GW)," Arya wrote. In his own note, Bernstein analyst Stacy Rasgon wrote that Broadcom's Google deal is incremental, noting that it could help, "ease customer owned tooling fears, as well as seemingly give a solid datapoint that both Broadcom and their largest customer believe they have substantial demand visibility far out into the future (or at least 5 years)." Broadcom stock has benefited handsomely from the AI boom, rising 110% over the last 12 months, but like many AI stocks has taken a step back since the start of the year, falling more than 6% during the period.

Anthropic Locks In Hundreds of Billions in Google and Broadcom Compute

This article first appeared on GuruFocus. Anthropic committed to "multiple gigawatts" of computing capacity from Google Cloud, a unit of Alphabet (GOOGL), including approximately 3.5 gigawatts to be delivered via a new agreement with Broadcom (NASDAQ:AVGO), starting in 2027. Total new capacity across the agreements could reach close to 5 gigawatts, according to a person with knowledge of the terms. At an estimated $35 billion to $50 billion per gigawatt of infrastructure, the commitment could run to hundreds of billions of dollars. Broadcom shares rose 3.58% in premarket while Alphabet rose 1.32%. The chipmaker separately agreed to develop and supply future generations of Google's tensor processing units through 2031. Anthropic said its annualised revenue reached $30 billion at the end of March, up from approximately $9 billion at the end of 2025, a more than threefold increase in roughly three months. The number of enterprise customers each spending over $1 million annually has more than doubled to over 1,000 since February. "We are building the capacity necessary to serve the exponential growth we have seen in our customer base," said Krishna Rao, Anthropic's chief financial officer, in a company blog post. The commitment extends a series of infrastructure deals Anthropic has struck since late 2025, including a $50 billion data centre agreement with Fluidstack and $30 billion in capacity from Microsoft (NASDAQ:MSFT) and Nvidia (NASDAQ:NVDA).

Anthropic Forges Chip Deals to Accelerate Claude's Growth

Anthropic Forges Chip Deals to Accelerate Claude's Growth The deals are dependent on the vendor's commercial success. The generative AI vendor has entered into agreements with Google and chipmaker Broadcom to significantly grow its compute infrastructure and capacity. A blog on the vendor's website said the expansion was driven by a desire to further "power our frontier Claude models and help us serve extraordinary demand from customers worldwide." "Multiple" gigawatts of next-generation Google TPU (tensor processing unit) AI chips would be involved, as well greater use of the tech giant's cloud services. While the blog provided few details, a Securities and Exchange Commission filing from Broadcom gave more insight into what is included in the agreements. Starting in 2027, Broadcom would provide about 3.5 gigawatts of TPU-based compute capacity to Anthropic, according to the SEC filing. Broadcom manufactures and helps design TPUs for Google. Broadcom's TPUs chips rival Nvidia's hugely successful GPUs. Separately, the Broadcom filing also revealed that the firm has entered into a "long-term agreement" with Google to design and supply future TPU chips, plus signed a supply assurance agreement for "networking and other components" for use in Google's next-generation AI racks up to 2031. The 3.5 gigawatts comes on top of 1 gigawatt Broadcom is supplying Anthropic in 2026, as confirmed by Broadcom CEO Hock Tan in an earnings call in March. "This groundbreaking partnership with Google and Broadcom is a continuation of our disciplined approach to scaling infrastructure: we are building the capacity necessary to serve the exponential growth we have seen in our customer base while also enabling Claude to define the frontier of AI development," Anthropic CFO Krishna Rao said in a statement. While no financials were confirmed, the capacity and hardware involved means the cost is likely to stretch to hundreds of billions of dollars. Given that Anthropic has not yet made a profit and is racking up sizeable financial losses, despite heavy funding, Broadcom said in the filing that the deal was contingent on "Anthropic's continued commercial success" and that the parties involved were "in discussions with certain operational and financial partners." However, Rao, while acknowledging that the deal was Anthropic's "most significant commute commitment yet," provided figures to illustrate the company's growth and massive potential. He revealed that its run rate revenue had now surpassed $30 billion -- up from $9 billion at the end of 2025. He also said the number of business customers now spending more than $1 million a year with Anthropic has doubled from 500 to 1,000 since February.

SpaceX IPO Targets $75 Billion, Allocating Up to 30% of Shares to Retail Investors - FinanceFeeds

SpaceX is preparing to allocate an unusually large portion of its upcoming IPO to retail investors, according to details shared with its banking syndicate. The plan marks a departure from traditional public offerings, where retail participation is typically limited to a small fraction of total shares. At a meeting with bankers, the company indicated that retail investors will play a central role in the offering, with a dedicated event planned to host 1,500 individuals in June following the IPO roadshow launch. "Retail is going to be a critical part of this and a bigger part than any IPO in history," Chief Financial Officer Bret Johnsen said during the meeting, according to people familiar with the discussion. He added that the approach is intentional, noting that these investors have been long-term supporters of both the company and its founder. Founder Elon Musk has previously pushed for allocating up to 30% of shares to smaller investors, compared with the 5% to 10% range typical in most IPOs. The IPO is expected to raise around $75 billion, implying a valuation of up to $1.75 trillion. If achieved, this would make it the largest initial public offering on record. The company plans to launch its roadshow in the week of June 8, with meetings scheduled between executives, bankers, and institutional investors. A group of approximately 125 analysts from the 21 participating banks is expected to meet with SpaceX ahead of the roadshow. Retail investors across multiple regions, including the US, UK, EU, Australia, Canada, Japan, and Korea, are expected to have access to the offering. The structure of the deal and the final size of the retail allocation are still being finalized, with more details expected closer to the IPO launch. The company is also preparing to publish its prospectus in late May. The targeted valuation represents a sharp increase from recent private market benchmarks. SpaceX was valued at around $800 billion in its December 2025 tender offer, which allowed employees and existing investors to sell shares in the secondary market. The company's valuation rose further after its merger with Musk's artificial intelligence venture xAI earlier this year, bringing the combined valuation to approximately $1.25 trillion. The IPO target of $1.75 trillion would extend that trajectory, reflecting expectations of continued growth across launch services, satellite infrastructure, and related technologies. SpaceX's approach signals a potential shift in how large technology IPOs are structured. By expanding retail access across multiple regions and dedicating a substantial share of the offering to individual investors, the company is testing whether broader participation can coexist with large-scale capital raising. One of the lead underwriters indicated that the scale of retail demand and allocation could exceed anything previously seen in public markets. Major banks, including Morgan Stanley, Bank of America, Citigroup, JP Morgan, and Goldman Sachs, are leading the deal, supported by 16 additional institutions covering global distribution channels. The outcome of the offering may influence how future high-profile listings balance institutional and retail demand, particularly if the structure affects pricing efficiency or post-listing liquidity.

Elon Musk Net Worth 2026: $811B Fortune, SpaceX IPO & Path to $1 Trillion

Elon Musk is not just the richest person alive. He is in a wealth category that has never existed before. At an estimated $811 billion according to the Forbes real-time tracker, Musk's fortune exceeds the GDP of countries like the Netherlands and Switzerland. He crossed $500 billion in October 2025, blew past $600 billion two months later, and hit $800 billion by February 2026 after merging SpaceX with xAI in the largest corporate combination in history. The speed of this wealth accumulation has no precedent. It took Jeff Bezos roughly a decade to go from first-time billionaire to $200 billion. Musk went from $500 billion to $800 billion in four months. And with SpaceX filing for a $1.75 trillion IPO that could close in late summer 2026, Musk is on track to become the world's first trillionaire before the year is out. Here is exactly how Musk's fortune breaks down, what is driving it, and why the numbers may be both more impressive and more fragile than they appear. The Wealth Breakdown: Where the $811 Billion Comes From Musk's net worth is concentrated in three assets. The combined SpaceX-xAI entity, Tesla stock, and X Holdings (formerly Twitter) account for virtually all of it. Everything else, Neuralink, The Boring Company, personal real estate, amounts to a rounding error at this scale. Musk's Asset Portfolio The composition has shifted dramatically in the past year. As recently as mid-2025, Tesla accounted for roughly 60% of Musk's wealth. Today, the SpaceX-xAI combination represents about 65%. This shift matters because SpaceX is private, meaning Musk's dominant asset is valued by private market transactions rather than public market trading, where valuations tend to be more generous and less volatile on a day-to-day basis. SpaceX-xAI: The $1.25 Trillion Merger That Changed Everything On February 2, 2026, Musk merged SpaceX and xAI in an all-stock deal that valued the combined entity at $1.25 trillion. SpaceX was valued at $1 trillion, xAI at $250 billion. The deal was structured as a share exchange, with each xAI share converting into 0.1433 SpaceX shares. Musk described the rationale as building "the most ambitious, vertically-integrated innovation engine on (and off) Earth." The practical reason was simpler: xAI was burning cash rapidly trying to compete with OpenAI and Anthropic, and SpaceX had the balance sheet and infrastructure to absorb it. The merger also enables Musk's vision of orbital data centers, where SpaceX's launch capabilities and Starlink's satellite network provide the physical infrastructure for xAI's computing needs. SpaceX-xAI: Key Numbers If the IPO prices at $1.75 trillion, Musk's 42% stake would be worth roughly $735 billion from this single asset alone, enough to push his total net worth past the $1 trillion mark even without any gains from Tesla. For a full breakdown of the IPO timeline, SEC filing details, and how retail investors can participate, see our deep-dive: SpaceX IPO 2026: $1.75 Trillion Valuation, SEC Filing, Timeline & How to Invest. Tesla: The Stock That Started It All Tesla shares closed at $352.82 on April 4, 2026, giving the company a market cap of approximately $1.14 trillion. Musk holds roughly 13% of outstanding shares, worth about $148 billion. But the more consequential piece is his 2018 compensation package: 304 million stock options with a $23.33 strike price. The Delaware Supreme Court restored this pay package in December 2025, reversing the lower court's Tornetta decision that had voided it. At the current stock price, those options carry an intrinsic value of approximately $115 billion ($352.82 minus $23.33, multiplied by 304 million shares). Combined with his direct equity, Musk's total Tesla exposure is roughly $263 billion. But Tesla's contribution to Musk's wealth story has shifted from growth engine to risk factor. The stock is down approximately 45% from its December 2024 peak of $479 per share. Q1 2026 profits dropped 71%. A Yale study found that Musk's political activities cost Tesla between 1 million and 1.26 million US vehicle sales, while boosting competitors by 17% to 22%. For a complete analysis of where TSLA may be headed, including robotaxi catalysts, Optimus timeline, and analyst price targets through 2030, see our Tesla Stock Price Prediction 2026-2030. Tesla's Recent Financial Trajectory The DOGE Factor: Politics as a Wealth Headwind Musk's role as head of the Department of Government Efficiency (DOGE) under President Trump has been the most polarizing chapter of his public life. While the position gave him influence over federal spending, it came at measurable cost to his core business. Tesla stock soared to $479 by mid-December 2024 on post-election optimism, then lost 45% of its value as consumer backlash intensified. Dealerships were vandalized. European sales cratered. Surveys showed 57% of American adults holding a negative view of Musk personally. Tesla's own earnings filings acknowledged that "political sentiment" could hurt the company. In April 2026, Musk announced he would step back from DOGE to refocus on Tesla, reducing his government role to one or two days per week. Tesla shares rose over 5% on the news, a telling indicator that the market had been pricing in DOGE as a liability rather than an asset. The tension at the heart of Musk's wealth is that his political influence and his commercial value pull in opposite directions. The same visibility that gave him a seat at the White House table drove away customers who buy electric vehicles. Whether the DOGE chapter ends up as a net positive (regulatory access, government contracts) or net negative (brand damage, lost sales) will not be clear for years. The Net Worth Milestones: A Timeline Without Precedent The pattern is striking. It took Musk three years to go from $300 billion to $400 billion (a period that included the Twitter acquisition, Tesla's stock decline, and public controversies). Then it took just four months to go from $500 billion to $800 billion. The acceleration is almost entirely driven by private market revaluations of SpaceX and xAI, not public market Tesla gains. The Path to $1 Trillion Fortune published a headline on April 2, 2026, calling Musk the "world's first trillionaire" based on implied SpaceX IPO valuations. That is premature. The IPO has not priced. But the math is straightforward. Trillionaire Scenarios If SpaceX prices at $1.75 trillion and Tesla holds current levels, Musk crosses the trillion-dollar threshold. Even at a $1.5 trillion IPO, he falls just short at roughly $919 billion, though any Tesla appreciation or Neuralink revaluation could close the gap. The bear case is that public markets value SpaceX more conservatively than private rounds have, the IPO prices at a discount to the S-1 target, and Tesla continues to slide. In that scenario, Musk remains comfortably above $800 billion but the trillionaire milestone moves to 2027 or later. Musk vs. the World: Wealth in Context Musk is not merely the richest person in the world. He is richer than the next four wealthiest people combined. His fortune is within striking distance of Saudi Arabia's annual GDP. This concentration of wealth in a single individual has no historical parallel in inflation-adjusted terms. The Risks Nobody Is Pricing SpaceX-xAI IPO execution risk. The $1.75 trillion valuation target assumes markets remain receptive to mega-cap tech IPOs. If market conditions deteriorate, the IPO could be delayed or downsized, freezing Musk's largest asset at a private valuation that may not reflect public market pricing. Tesla brand erosion may be structural, not cyclical. The Yale study documenting 1 million lost sales is not a temporary blip. Brand damage in the automotive industry tends to compound. Once consumers associate a brand with political controversy, recapturing them is harder than acquiring them in the first place, especially as competitors like BYD, Rivian, and legacy automakers improve their EV offerings. Private market valuations are not liquid wealth. Roughly 65% of Musk's fortune is in SpaceX-xAI, a private entity. He cannot sell shares freely. The IPO will create liquidity, but lock-up periods typically prevent founders from selling for 90 to 180 days after listing. Musk's paper wealth and his available capital are two very different numbers. Regulatory and litigation exposure. Musk faces ongoing SEC scrutiny over Tesla disclosures, FTC investigations into X (formerly Twitter), European regulatory pressure on content moderation, and potential conflicts of interest from his DOGE role. None of these are existential individually, but collectively they create an environment where a single adverse ruling could trigger a sentiment shift across his public and private holdings. Key-man risk is the highest in corporate history. No individual has ever had an $800 billion fortune tied so directly to their personal involvement in so many companies simultaneously. Tesla, SpaceX, xAI, X, Neuralink, The Boring Company. Musk's time is the scarcest resource in his empire, and DOGE demonstrated what happens when his attention is diverted from the core business. For more on the best AI stocks to buy in 2026 and where xAI, Nvidia, and other players fit into the broader landscape, explore our investment guides. What is Elon Musk's net worth in 2026? As of April 2026, Elon Musk's net worth is estimated at $811 billion according to the Forbes real-time billionaire tracker. The Bloomberg Billionaires Index puts the figure lower at approximately $636 billion due to differences in how private company stakes are valued. The discrepancy stems primarily from different valuations applied to SpaceX-xAI, which represents about 65% of Musk's fortune. How did Elon Musk get so rich so fast? Musk's wealth accelerated dramatically in late 2025 and early 2026 due to three events: Tesla's stock rally to $479 in December 2024, the Delaware Supreme Court restoring his $115 billion Tesla compensation package in December 2025, and the SpaceX-xAI merger in February 2026 that valued the combined entity at $1.25 trillion. He went from $500 billion to $800 billion in just four months. Will Elon Musk become a trillionaire? It depends primarily on the SpaceX IPO. If SpaceX-xAI prices at the targeted $1.75 trillion valuation in its expected late summer 2026 IPO, Musk's 42% stake alone would be worth roughly $735 billion. Combined with his Tesla holdings (~$263 billion), that would push his total net worth past $1 trillion. If the IPO prices below $1.5 trillion or Tesla continues to decline, the trillionaire milestone likely moves to 2027. What is the SpaceX-xAI merger? On February 2, 2026, SpaceX absorbed xAI in an all-stock deal valuing the combined company at $1.25 trillion (SpaceX at $1T, xAI at $250B). The merger created the most valuable private company in history. Musk described the rationale as building orbital data centers and a vertically-integrated AI and space infrastructure platform. SpaceX subsequently filed a confidential S-1 for an IPO targeting a $1.75 trillion valuation. Has DOGE hurt Elon Musk's wealth? Yes, measurably. Tesla stock fell roughly 45% from its December 2024 peak, with Musk himself acknowledging that DOGE backlash was hurting the stock. A Yale study found his political activities cost Tesla between 1 million and 1.26 million US vehicle sales. Consumer surveys show 57% of Americans now view Musk negatively. However, SpaceX and xAI valuations continued rising during this period, so the net impact on total wealth was partially offset by private market gains. Disclosure: This article is for informational purposes only and does not constitute investment advice. The author and TECHi may hold positions in securities mentioned. Always conduct your own research or consult a licensed financial advisor before making investment decisions. Net worth estimates vary by source and methodology; figures cited are as of the date published and subject to change.

Polymarket Rebuilds Its Trading 'Plumbing' with New Stablecoin & Faster Exchange Stack

In an announcement posted on X on Monday, Polymarket said it's rolling out what it described as its biggest infrastructure change since the decentralized prediction market's launch back in 2020. The changes include a rebuilt trading engine, updated smart contracts, and a new collateral token called Polymarket USD. Over the next two to three weeks, the event contract exchange will overhaul its core infrastructure to improve execution speed, lower gas costs, and create a cleaner technical foundation going forward. The most visible change for the platform's regular users will be the move from USDC.e to Polymarket USD, which the company says is backed 1:1 by USDC. In other words, Polymarket will replace the token users post as collateral with its own wrapper around USDC, while also upgrading the system that matches trades behind the scenes. Most of the changes to the front end will be handled automatically, the company said. However, open orders will be canceled for a short time during the maintenance window, which will be announced at least a week in advance. What the Upgrade Actually Changes From a technical perspective, Polymarket is launching CTF Exchange V2 and a new version of its central limit order book, or CLOB. If you're not familiar with the crypto space, these changes basically mean faster trade matching, lower transaction costs, and updated rails for bots, apps, and other tools that plug into the exchange. The company also said the new stack will support EIP-1271 signatures, a change that should make it easier for smart contract wallets to interact with the platform. The upgrades go beyond the retail trading experience. In a post on X explaining the update, Polymarket Developers said API traders, bot operators, and other integrators will need to update their software development kits and re-sign orders using the new structure. TypeScript, Python, and Go clients are expected to be ready before release day, with migration docs and a full API changelog still to come. Upgrade Follows a String of Infrastructure Deals Polymarket's April 6 announcement follows several moves by the company in early 2026 to strengthen the technical infrastructure behind its exchange. The company has spent the past few months building out its core technology through a series of acquisitions and major funding rounds. * February 19: Polymarket acquired Dome, a Y Combinator-backed startup that specializes in unified API infrastructure, to streamline how third-party tools access market data. * March 18: The company purchased Brahma, a DeFi infrastructure specialist, to improve wallet creation, cross-chain operations, and token redemptions. * March 27: Intercontinental Exchange (ICE), the parent company of the New York Stock Exchange, completed a $600 million direct cash investment in Polymarket. This followed ICE's $1 billion investment in late 2025. As Polymarket integrates these specialized technologies and secures significant institutional backing, it's increasingly positioning itself as more than a typical betting platform. The new infrastructure gives Polymarket the core trading "plumbing" it needs to reduce its reliance on third-party providers, allowing it to create a more stable, scalable environment as it continues its CFTC-regulated re-entry into the United States market.

Broadcom expands Google, Anthropic deals; Intel joins Musk's Terafab

Market Catalysts host Julie Hyman takes a look at some of Tuesday morning's trending tickers and stories. Shares of health insurers, including UnitedHealth (UNH), Humana (HUM), and CVS (CVS), are soaring on news that the government will increase private insurer reimbursements by 2.48%. Broadcom (AVGO) is expanding its deals with Google (GOOG, GOOGL) and Anthropic (ANTH.PVT). Intel (INTC) is set to join Elon Musk's Terafab artificial intelligence (AI) chip project with Tesla (TSLA), SpaceX, and xAI.

Broadcom expands Google, Anthropic deals; Intel joins Musk's Terafab

Market Catalysts host Julie Hyman takes a look at some of Tuesday morning's trending tickers and stories. Shares of health insurers, including UnitedHealth (UNH), Humana (HUM), and CVS (CVS), are soaring on news that the government will increase private insurer reimbursements by 2.48%. Broadcom (AVGO) is expanding its deals with Google (GOOG, GOOGL) and Anthropic (ANTH.PVT). Intel (INTC) is set to join Elon Musk's Terafab artificial intelligence (AI) chip project with Tesla (TSLA), SpaceX, and xAI.

Intel says to join the Terafab project with SpaceX, xAI and Tesla

This super composite rating is the result of a weighted average of the rankings based on the following ratings: Fundamentals (Composite), Global Valuation (Composite), EPS Revisions (1 year), and Visibility (Composite). We recommend that you carefully review the associated descriptions. This composite rating is the result of an average of the rankings based on the following ratings: Fundamentals (Composite), Valuation (Composite), Financial Estimates Revisions (Composite), Consensus (Composite), and Visibility (Composite). The company must be covered by at least 4 of these 5 ratings for the calculation to be performed. We recommend that you carefully review the associated descriptions.

BB's Stock Haven : SpaceX A multi-division aerospace and c...

The purest play: Why Boron One is THE boron stock to own While dozens of minerals are considered critical to economic and national security, thanks to their combination of scarcity and unmatched industrial performance, few minerals, if any, are more ubiquitous across the industrial landscape than boron. Let's paint a picture: Perhaps most urgently, boron is also an essential component across the renewable energy industry, making it [...]

Drunk passenger who caused chaos on flight to UK sentenced

A man, who was intoxicated on a flight from Poland to the UK, has been sentenced. Stephen Blofield, 61, from Haverfordwest, pleaded guilty in February to several charges. These included being drunk on an aircraft, behaving in a threatening, abusive, insulting, or disorderly manner towards a member of the aircraft crew, using threatening or abusive words or behaviour likely to cause harassment, alarm, or distress, and failing to obey lawful commands of the pilot while onboard the aircraft. The offences relate to a flight on Tuesday 11 November from Krakow to Bristol Airport. Stephen Blofield, 61, from Haverfordwest, pleaded guilty. (Image: Avon and Somerset Police) He was sentenced at Bristol Crown Court to 10 months in prison today (Tuesday 7 April). Blofield must also pay a victim surcharge of £187. Inspector Christian Gresswell, of the Bristol Airport policing team, said: "Passengers have a duty for safety reasons to make sure they are fit enough to fly and not intoxicated. "Stephen Blofield caused the initial landing to be aborted and continued to be verbally abusive towards cabin crew. He was met by officers at Bristol Airport once the flight had safely landed. "We want people travelling to and from a holiday to relax and enjoy themselves, but we hope this case serves as a bit of a reminder to people that everyone needs to take responsibility for their own actions and ensure they are in a fit state to fly. An intoxicated passenger can pose an unacceptable risk to safety, and that's why we take the offence so seriously. "We will continue to work closely with airport staff and airlines to keep passengers and crew safe at all times."

Kremlink: Is Russia Trying to Build Its Own SpaceX? | UACRISIS.ORG

On March 23, 2026, Russia launched 16 satellites of the Rassvet system from the Plesetsk Space Center. The "Rassvet" low-Earth orbit broadband satellite system project, implemented by Bureau 1440, is a key element in the Kremlin's strategy to achieve "digital sovereignty." At the same time, Russian official media are interpreting the event as the launch of Russia's own version of Starlink. On the other hand, its current political and media significance far exceeds the actual level of deployment, as key questions regarding scalability, the cost of the ground segment, and the network's actual bandwidth remain unresolved. As of the present, the launch of the first batch of satellites does not yet signify the emergence of a fully-fledged and sustainable broadband communication system. At this stage, it is more a demonstration of intent and technological ambitions than the creation of a ready-made infrastructure capable of providing Russia with an autonomous communication channel in both the military and civilian sectors. The Kremlin's Ambitions The "Rassvet" project is Russia's attempt to build a low-Earth orbit constellation that could partially reduce its dependence on Western digital platforms and communication channels. The system operates on low-Earth orbit (LEO) satellites at an altitude of 500-800 km, which reduces signal latency to 38-42 ms. This is considered the necessary standard for modern network protocols and real-time systems. Key technological innovations include the integration of 5G NTN (Non-Terrestrial Networks) architecture, which allows satellites to act as base stations in orbit, and the use of intersatellite laser links (ISL) to transmit terabytes of data without the involvement of ground-based gateway stations. A proprietary satellite system could potentially allow Russia to deploy a secure military messaging network and geospatial data exchange systems that would be isolated from the global internet. As of March 2026, the project has moved from the experimental stage (the "Rassvet-1" and "Rassvet-2" missions) to the serial deployment of the target constellation. According to Russian authorities, the "Rassvet" system is a response to the critical dependence on Western technology that became apparent during the invasion of Ukraine. Therefore, the Russian authorities plan to transform "Rassvet" into a secure communications network that could eventually be used for military command and control, data exchange with unmanned systems, and long-distance infrastructure support. Meanwhile, "Bureau 1440" has already unveiled prototypes of terminals for rail transport capable of providing stable connectivity at speeds of up to 400 km/h. Memorandums have also been signed with Aeroflot regarding the installation of terminals on aircraft by 2028. Russia's "space internet": yet another costly myth? Over the next two years (2026-2027), the key indicator of the project's success will be Russia's ability to launch the promised 250+ satellites into orbit and begin commercial operations. If "Bureau 1440" can establish mass production of low-cost subscriber terminals, Russia will gain a tool for influence both domestically and in various regions of the world, effectively creating an alternative "space internet" (alongside China's "Qianfang" satellite system) free from American control. Otherwise, the project risks remaining an expensive state initiative with a limited user base within law enforcement agencies. The criticism, which came not only from Ukrainian or Western sources but also from within the Russian military community itself, deserves special attention. Following issues with access to Telegram and the general vulnerability of battlefield communications in 2026, some military correspondents and pro-war commentators directly asked what exactly the Russian army intends to use to replace the usual coordination channels on the front lines. What is significant in this criticism is not only the emotional tone but also the substance of the accusation: Russian authors effectively acknowledged that while the state declares a commitment to digital sovereignty, it lacks a fast, widespread, and accessible solution for combat units. Another striking motive behind this criticism is the gap between the public display of a "space breakthrough" and the reality on the front lines. Even commentators loyal to the regime have pointed out that grandiose statements about a future orbital network do not solve the current problem of tactical communications. In other words, the skepticism of part of the Z-community is rooted in doubts about the Russian state's ability to quickly transform an expensive image-building project into a functional tool for the military. The ground segment remains the project's weakest link. For satellite internet to become widespread, the price of the terminal must be affordable for the average citizen or small business. The stated cost of 50,000 rubles for individuals seems overly optimistic. This leads to a more cautious assessment of the project's international prospects. If "Rassvet" cannot provide a relatively inexpensive subscriber terminal, stable bandwidth, and reasonable scaling timelines, its potential as a foreign policy tool will be limited. In that case, the system will remain not so much a global alternative to Western networks as an expensive state-run communications network for select users -- primarily the security forces. Ultimately, "Rassvet" should be viewed not as a fully-fledged alternative to Starlink, but as an attempt to create a counterpart under the pressure of war, technological constraints, and the nation's dependence on external communication channels. The launch of production satellites itself shows that this project is not merely declarative and does indeed have political priority and resource support. At the same time, as of today, this is more about the beginning of a long, expensive, and technically vulnerable process, the outcome of which is not yet guaranteed, and the practical value of the system for military and civilian tasks remains an open question.

Anthropic Revenue Tops $30 Billion as Google and Broadcom Sign Multi-GW TPU Deals

Surging demand for advanced AI models is reshaping cloud infrastructure, energy markets, and Bitcoin mining economics, with anthropic revenue emerging as a key signal of this shift. Anthropic disclosed that its annualized revenue has climbed past $30 billion, a sharp acceleration from approximately $9 billion at the end of 2025. This jump in anthropic annual revenue reflects rapid uptake of its Claude AI models across enterprise clients and software developers. Moreover, the company is seeing strong demand from large organizations integrating Claude into workflows, products, and internal tooling. The firm also reported that the number of business customers spending more than $1 million per year on Claude has doubled in under two months, rising from 500 to more than 1,000. That said, Anthropic has framed this as an early stage of broader enterprise AI adoption, suggesting significant room for further growth as organizations scale deployments. To sustain this trajectory, Anthropic announced long-term infrastructure agreements with Google and Broadcom for several gigawatts of next-generation TPU (Tensor Processing Unit) compute capacity. The new infrastructure is expected to begin coming online in 2027 and will be used to train and operate future versions of Claude. However, the scale of the deal also underscores how dedicated AI hardware is now central to performance and competitive advantage. Anthropic revealed that it has secured roughly 3.5 gigawatts of next-generation Google TPU capacity through Broadcom starting in 2027. This commitment is in addition to about 1 gigawatt of Google compute that Anthropic is already slated to receive in 2026. Together, these agreements signal a multiyear build-out of specialized infrastructure to support increasingly capable models. Across the sector, major AI developers are racing to lock in long-term access to training and inference capacity. Moreover, the combination of Google's TPU ecosystem and Broadcom's semiconductor design and manufacturing capabilities positions them as critical suppliers in this expanding market. These moves highlight broader ai hardware partnerships trends that are reshaping the cloud and chip landscape. The surge in anthropic revenue is closely tied to the company's ability to secure massive cloud compute deals and scale next-generation models. With multi-year TPU capacity in place, Anthropic is positioning itself to expand Claude's capabilities while maintaining competitive performance. Furthermore, the agreements illustrate how compute availability is becoming a primary constraint on AI growth, rather than model design alone. Market implications include rising enterprise demand for AI services, increasing capital intensity, and the growing strategic importance of hardware suppliers. As AI adoption spreads, access to low-cost, high-density compute is emerging as a key differentiator between leading AI labs and smaller competitors. This dynamic is likely to influence anthropic revenue growth and shape industry structure over the next several years. The rapid build-out of AI infrastructure is directly competing with Bitcoin mining for scarce physical resources such as grid connections, land, cooling capacity, and low-cost electricity. According to Cambridge tracking data, global Bitcoin mining continuously consumes an estimated 13 to 25 gigawatts of power. However, a single Anthropic deal delivering multiple gigawatts of demand shows that AI has become one of the largest new electricity users in the United States. Several publicly listed Bitcoin mining companies are now pivoting toward ai hosting bitcoin miners strategies and high-performance computing to secure stable, contracted revenue. Examples include large conversions of mining facilities into AI data centers and long-term hosting agreements with Anthropic and other AI customers. Moreover, mining economics have come under pressure, with some operators facing loss-making conditions at current BTC prices, while AI hosting offers predictable cash flows backed by enterprise contracts. Analysts estimate that a substantial share of mining companies' revenue could come from AI and high-performance computing by the end of the year. In aggregate, more than $70 billion in cumulative AI and HPC deals has been announced across the public mining sector. This capital reallocation underscores how AI demand is reshaping the business models of traditional mining players. The power grid is coming under increasing stress from concentrated data center demand, including large AI clusters. Grid operators in the United States project capacity shortfalls in coming years, while industry studies forecast U.S. data center electricity demand rising sharply through 2030. Moreover, single facilities reaching 1 gigawatt of load can rival the consumption of small cities, intensifying local constraints. Many announced data center projects are already facing delays tied to power limitations and shortages of critical grid equipment. Anthropic's multi-gigawatt commitment to new AI capacity enters this constrained environment, heightening competition for grid access, substations, and transmission upgrades. As a result, data center power demand is increasingly a central issue for regulators, utilities, and technology firms. Over the past decade, Bitcoin miners have assembled portfolios of remote sites with favorable power purchase agreements, large grid connections, proximity to substations, and substantial cooling capacity and land. Now, these assets align closely with AI deployment needs. Consequently, many miners are converting mining facilities into data centers for AI customers and repositioning themselves as infrastructure landlords with long-duration leases and institutional tenants. This strategic shift carries important implications for the Bitcoin network. Large miners are monetizing BTC holdings to finance AI conversions, adding sell pressure to spot markets. Moreover, as mining capacity is redirected toward AI workloads, Bitcoin hash rate and mining difficulty can decline, at least temporarily, affecting short-term network security metrics. Over the longer term, the publicly listed mining sector may increasingly resemble diversified infrastructure operators. They could focus on leasing power, space, and uptime to AI companies while mining opportunistically when economics are favorable. That said, the pace and scale of this transition will depend on relative returns from AI hosting versus traditional block-reward mining. Broadcom separately announced an extended partnership with Google to design and supply future generations of specialized AI processors and related technologies through 2031. Broadcom has long manufactured Google's TPUs and confirmed that it is expanding deliveries. The company indicated it was already supplying approximately 1 gigawatt of computing power in 2026 and expects demand to exceed 3 gigawatts by 2027. Analyst estimates suggest a significant AI-driven revenue opportunity for Broadcom tied to these long-term agreements. Moreover, Broadcom is also involved in custom processor design programs with other major AI developers, extending its reach across the gpu tpu trainium hardware stack. Google's partnership with Broadcom on google broadcom tpu capacity reinforces the strategic importance of bespoke accelerators for leading cloud and AI providers. Anthropic has emphasized that it trains and runs Claude across a range of hardware platforms, including AWS Trainium processors, Google TPUs, and Nvidia GPUs. This diversified approach aims to optimize performance, cost, and resilience while tapping different cloud ecosystems. Furthermore, the company has signaled plans for substantial investment in U.S. computing infrastructure as it scales next-generation models. The combination of rapid revenue growth, large-scale TPU commitments, and a multi-vendor hardware strategy shows how compute capacity is becoming a core driver of growth and differentiation in the AI industry. In this environment, Anthropic's agreements with Google and Broadcom, alongside its broader cloud relationships, position the company to compete aggressively for enterprise AI workloads over the coming decade. In summary, Anthropic's soaring revenue, multi-gigawatt compute deals, and the sector-wide shift toward AI hosting highlight how advanced models are reshaping infrastructure, energy demand, and even the economics of Bitcoin mining.

Polymarket Launches PolymarketUSD: A New Stablecoin to Power Its Prediction Market Exchange - Blockonomi

Builders must update to the latest CLOB-Client SDK in TypeScript, Python, or Go and re-sign all orders. Polymarket, the largest prediction market platform, is set to launch its own collateral token, PolymarketUSD. The new token will replace USDC.e as the platform's primary trading currency. Backed 1:1 by USDC, the transition aims to optimize the exchange's infrastructure. This move forms part of a broader platform upgrade affecting contracts, order books, and the collateral system. Most users will experience the change without manual intervention. Polymarket USD will serve as the new collateral token across the platform's trading environment. The token maintains a direct 1:1 backing with USDC, preserving value stability for all participants. For most users, the frontend will handle the wrapping process automatically through a one-time approval prompt. However, power users and API-only traders face a different requirement during this migration. They must wrap their USDC or USDC.e manually into PolymarketUSD. This is done through the Collateral Onramp contract's wrap() function, which handles the conversion directly onchain. The migration timeline spans two to three weeks, covering the full exchange stack. Polymarket has confirmed it will announce the exact maintenance window at least one week before the upgrade goes live. During that window, all existing order books will be cleared entirely. This collateral change connects directly to the broader CTF Exchange V2 upgrade. The new exchange contract introduces optimized order structures, better matching logic, and support for EIP-1271 signatures. Fee collection and distribution have also been streamlined under the updated architecture. Beyond the token migration, Polymarket is rolling out a new CLOB-Client SDK to support the V2 infrastructure. TypeScript, Python, and Go clients will all receive updated versions ahead of release day. Builders running bots or integrations must update their SDK and re-sign orders using the new order struct. The new SDK handles the V1-to-V2 transition automatically, but only for builders running the latest client version. Each client queries a version endpoint and refreshes on migration day without manual input. Documentation and migration guides will be shared before the release date. CTF Exchange V2 also introduces builder codes, which allow onchain attribution for order flow. This addition gives builders a structured way to track activity tied to their integrations directly onchain. It marks a notable step toward greater transparency for programmatic market participants.

Elon Musk's xAI Rivalry Sparks OpenAI Legal Action and State Investigation Request

OpenAI has asked state officials in California and Delaware to investigate Elon Musk and his associates for what it calls "improper and anti-competitive behavior," as a major court battle between the two sides nears. In a letter sent Monday to California Attorney General Rob Bonta and Delaware Attorney General Kathy Jennings, OpenAI claimed Musk's actions could harm fair competition and disrupt its mission. The request comes just weeks before a jury trial expected to begin later this month in California. The dispute traces back to Musk's lawsuit filed in 2024 against OpenAI and its CEO, Sam Altman. Musk accused the company of moving away from its original nonprofit mission as it shifted toward a for-profit structure. Musk, who co-founded OpenAI in 2015, left the group in 2018 and later launched rival AI company xAI, which created the chatbot Grok, Reuters reported. OpenAI said Musk's lawsuit is seeking more than $100 billion in damages from its nonprofit foundation, a move it warned could seriously damage the organization. A judge has already ruled that the case will go before a jury. Jason Kwon, OpenAI's chief strategy officer, said in the letter that Musk's actions may interfere with the company's goal of developing artificial general intelligence, or AGI, for public benefit. "These attacks are designed to take control of the future of AGI out of the hands of those who are legally obligated to pursue the mission of ensuring that AGI benefits all of humanity," Kwon wrote. The company also raised concerns about alleged coordination between Musk and Mark Zuckerberg, though it said Zuckerberg did not join a past investment bid tied to Musk's group. OpenAI further pointed to reports claiming that individuals linked to Musk gathered information about Altman and spread harmful claims. It argued that such actions show a pattern of behavior that should be reviewed by regulators. Chris Lehane, OpenAI's chief global affairs officer, questioned why powerful tech leaders would try to block the company's progress. According to CNBC, he said their actions are "highly questionable and sharply worthy of investigation." The company also warned that if Musk succeeds in court, it could benefit xAI's Grok platform, which has faced scrutiny over its outputs. Musk has not publicly responded to the latest claims.

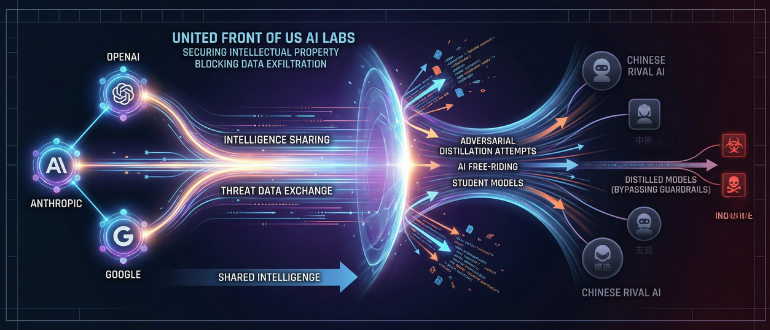

OpenAI, Anthropic, Google Form United Front to Block Chinese 'AI Free-Riding' - Techstrong.ai

Rivals OpenAI, Anthropic, and Google have begun sharing sensitive intelligence to thwart Chinese competitors from distilling their artificial intelligence (AI) models in a rare alliance to protect their intellectual property. The collaboration, facilitated through the Frontier Model Forum -- an industry nonprofit founded in 2023 -- marks a significant escalation in the global AI arms race. According to a Bloomberg report, citing people familiar with the matter, the firms are swapping data to detect "adversarial distillation," a process where users extract outputs from top-tier U.S. models to train cheaper, imitation versions. The stakes are both economic and existential. U.S. officials estimate that unauthorized distillation costs Silicon Valley labs billions of dollars in annual profit. By using a "teacher" model from the U.S. to train a "student" model in China, developers can replicate high-level reasoning capabilities at a fraction of the original research and development cost. The urgency behind the partnership intensified following the January 2025 release of DeepSeek-R1. The Chinese startup's model shocked the industry by matching the performance of U.S. systems while remaining "open-weight" and significantly cheaper to operate. OpenAI recently escalated the rhetoric in a memo to Congress, explicitly accusing DeepSeek of trying to "free-ride on the capabilities developed by OpenAI and other U.S. frontier labs." While DeepSeek has maintained its innovations are original, Microsoft and OpenAI launched internal investigations into whether the Chinese firm exfiltrated massive datasets to build its reasoning engine. Beyond the loss of market share, U.S. labs warn of a "guardrail gap." While proprietary U.S. models like GPT-4 or Claude are programmed with strict safety limits to prevent the creation of biological weapons or the execution of cyberattacks, distilled models often bypass these filters. "The threat extends beyond any single company," Anthropic said recently, when it identified Chinese labs DeepSeek, Moonshot, and MiniMax as illicitly extracting capabilities. Without oversight, these distilled models could provide bad actors with high-level technical assistance for malicious activities. The industry's move mirrors cybersecurity protocols where firms trade data on hacking threats to bolster collective defenses. It also aligns with the Trump administration's AI Action Plan, which calls for an information-sharing center to curb foreign exploitation of U.S. tech. However, the collaboration remains in its early stages. Insiders suggest that while the companies are eager to protect their hundreds of billions in infrastructure investments, they are navigating a legal minefield. Many are seeking clearer guidance from the Department of Justice to ensure that sharing information about Chinese competitors does not run afoul of U.S. antitrust laws. As Chinese open-source models continue to proliferate, Silicon Valley is betting that its proprietary moats can only be maintained if the industry acts as a single entity to slam the door on data exfiltration.

Intel Joins Tesla's Terafab Chip Project With SpaceX and xAI

Intel announced on Tuesday that it has joined the Terafab semiconductor project alongside Tesla, SpaceX, and xAI -- formalising a partnership that Elon Musk first floated five months ago when he told shareholders it was "probably worth having discussions with Intel." The chipmaker said its ability to "design, fabricate, and package ultra-high-performance chips at scale" would help accelerate Terafab's goal of producing one terawatt of compute per year to power advances in artificial intelligence and robotics. "It was fun hosting @elonmusk at Intel this past weekend," the company wrote on X. As of press time, Tesla shares were trading 2.6% lower at $343.50. From 'Maybe' to Partnership Musk first raised the idea of working with Intel at Tesla's annual shareholder meeting on November 6, 2025. "You know, maybe we'll do something with Intel," Musk told shareholders. "We haven't signed any deal, but it's probably worth having discussions with Intel." Intel's stock jumped 4% in after-hours trading that day. At the time, Musk was laying out the scale of Tesla's chip problem. Even extrapolating the best-case scenario for production from existing suppliers -- TSMC and Samsung -- the output would not be enough to meet the combined needs of Tesla's Full Self-Driving system, Cybercab robotaxi fleet, and Optimus humanoid robot programme, he said. "I can't see any other way to get to the volume of chips that we're looking for," Musk said. "So I think we're probably going to have to build a gigantic chip fab. It's got to be done." That vision became Terafab four months later. What Intel Brings Intel is one of only three companies in the world -- alongside TSMC and Samsung -- with the capability to fabricate chips at advanced process nodes. It also possesses industry-leading packaging technologies, including Foveros 3D stacking and EMIB, which are critical for high-performance AI processors. The company has been seeking external customers for its foundry business after years of declining revenue and an $18.76 billion loss in 2024. The US government took a 9.9% stake in Intel last year, and the chipmaker has since secured investments from SoftBank ($2 billion) and Nvidia ($5 billion). Before Tuesday's announcement, Intel was already handling packaging for Tesla's Dojo 3 chips at its Arizona facility. Barclays had recently noted in its Terafab analysis that Intel fits Musk's preference for a US-based supply chain and "might have available capacity" -- making it a natural partner alongside Samsung and TSMC. What Terafab Is Terafab is a joint venture between Tesla, SpaceX, and xAI -- the AI company that SpaceX acquired in an all-stock deal in February. The project was announced on March 21, at a livestreamed event from the defunct Seaholm Power Plant in Austin, Texas. Musk called it "the most epic chip building exercise in history by far." The facility is designed to consolidate every stage of semiconductor production under one roof: chip design, lithography, fabrication, memory production, advanced packaging, and testing. A prototype "Advanced Technology Fabrication" facility will be built at the North Campus of Giga Texas, with the full-scale Terafab at a location yet to be determined. At full capacity, Tesla claims the output would match roughly 70% of TSMC's entire current global production. Terafab targets 2-nanometer process technology with an initial capacity of 100,000 wafer starts per month, scaling to one million. The project will produce two types of chips: an edge-inference processor -- the AI5, which Tesla claims delivers a 50x improvement over the current AI4 -- for FSD, Optimus robots, and Cybercab, and a radiation-hardened D3 variant for SpaceX's orbital AI satellites. Musk said 80% of compute output would be directed toward space applications. The estimated cost is $20-25 billion, which Tesla's CFO confirmed is not yet incorporated into the company's 2026 capital expenditure plan, which already exceeds $20 billion. Why It Matters for Tesla The Optimus robot programme is the largest single driver of chip demand. Morgan Stanley analyst Andrew Percoco estimated that Giga Texas alone could require 20 million chips per year for a capacity of 10 million humanoid robots -- approximately six times Tesla's current chip demand across its entire automotive business. Musk has said that all current global chip fabs combined produce roughly 2% of what his companies will eventually need. "We either build the Terafab or we don't have the chips, and we need the chips, so we build the Terafab," Musk said at the March event. Small-batch production of the AI5 chip is expected in late 2026, with volume production in 2027 -- though Tesla had already delayed the AI5 to mid-2027 before the Terafab announcement, and the AI6 chip has been delayed roughly six months due to Samsung's 2nm production slipping. Analyst Reaction Wedbush's Daniel Ives, one of Tesla's most vocal bulls, reiterated an Outperform rating and a $600 price target -- the highest on Wall Street -- following the Terafab announcement. He called the project "the first step to ultimately what will be Tesla and SpaceX combining forces in a merger likely in 2027," escalating a thesis Wedbush has been building since the SpaceX-xAI all-stock merger in February. Morgan Stanley's Percoco called Terafab a "Herculean task" and estimated the full cost could run $35-45 billion. He projected that initial chip output would not occur until mid-2028 at the earliest under an aggressive build-out scenario. Bernstein's Stacy Rasgon was more sceptical, stating that "a true Terafab feels like a stretch" and projecting that the full one-terawatt ambition could require $5-13 trillion in capital. Barclays' Dan Levy warned that the project could require spending "many multiples" above his own $50 billion bull-case estimate, calling the capital outlook "likely well more than an order of magnitude higher" than Tesla has communicated. Levy reiterated an Equalweight rating and $360 price target. He noted that Barclays forecasts Tesla's 2026 free cash flow at negative $3 billion before any Terafab-related spending. Precedents The scepticism is informed by Tesla's own track record on capital-intensive manufacturing pivots. At Battery Day in September 2020, Musk projected three terawatt-hours of annual in-house cell production by 2030. Five and a half years later, Tesla has reached roughly 2% of that target. The 4680 battery programme took years longer than promised, and Tesla's own top battery supplier publicly said Musk "doesn't know how to make battery cells." Tesla's Dojo supercomputer project, announced in 2021, was disbanded in August 2025 after Musk called it "an evolutionary dead end." It was revived in January 2026 as an orbital compute concept tied to SpaceX -- the same infrastructure Terafab is now designed to serve. Nvidia CEO Jensen Huang publicly cautioned Musk against underestimating the challenge, saying that matching TSMC's semiconductor capabilities is "virtually impossible." Tesla is scheduled to report first-quarter earnings on April 22, where capex guidance and Terafab funding details are expected to be addressed.

Here Comes SpaceX's IPO. Should You Board on Day One?

This post may contain links from our sponsors and affiliates, and Flywheel Publishing may receive compensation for actions taken through them. There's more to Elon Musk than just Tesla (NASDAQ:TSLA | TSLA Price Prediction) stock. And soon, retail investors will be able to get a piece of a company that may very well outshine the electric vehicle (EV) and robotics powerhouse. With EV sales and shares of Tesla under considerable pressure in April, perhaps there's no better time for another Musk-led firm to hit the private markets. With SpaceX combining with xAI, an AI firm that would be worth a fortune itself, the stage seems set for the biggest IPO of all-time, with a target valuation that might hit $2 trillion on the upside. That's not only big, but it will reshape the S&P 500 as we know it, given its top-heaviness. Any way you look at it, the stock market is about to move into a new era beyond the Magnificent Seven, as Elon Musk's rocket and AI company looks to change the world. With the Elon Musk premium attached, the rocket ship excitement factor, and the upside surrounding xAI's Grok as well as its different approach to AI, I certainly wouldn't be surprised if investors who don't get a seat on day one end up having to pay a price that implies a market cap well north of $2 trillion. As exciting as the businesses (from reusable rockets to AI chips for data centers in space) are, I view the name as more than a hype-driven titan. The company isn't just on the cutting-edge of tomorrow's tech; it's actually making money from industries (think SpaceX and Starlink) that the rest of the corporate world seems eager to break into. Of course, there are considerable barriers to entry when it comes to sending satellite payloads into space. The same goes for designing economical rockets. In any case, I think once SpaceX (SpaceX-xAI or whatever it'll be called) has the potential to be one of the more magnificent members of the Mag Seven. What's more, though, is that perhaps Tesla shareholders might have an escape hatch with the name. Why hang onto shares of a falling EV play when you can own a piece of one of the biggest game-changers in the private space market? And with Amazon (NASDAQ:AMZN) clashing with Apple (NASDAQ:AAPL) to acquire GlobalStar, a firm which Apple already owns a stake in, it certainly seems like the rest of the Mag Seven are following in SpaceX's lead. Space is the next frontier for mega-cap tech, and perhaps it's not too outlandish to see the SpaceX IPO take away much of the investment dollars from the seven tech titans. When it comes to economic moat width, SpaceX might be tops. And as it maintains its massive share of space, perhaps it's the Mag Seven that will need to pay Elon Musk and company for a ride to the stars or to use their satellite constellation. Who knows? If Apple is paying for Google Gemini, perhaps some of the tech firms out there will wind up paying SpaceX for its AI. In the meantime, though, xAI might be off-putting to some, especially since the market is no fan of AI CapEx these days. At a $1.75-2 trillion market cap? Probably not. Perhaps you'll get enough exposure by way of the Nasdaq 100 or S&P 500. As the biggest IPO to land, there's going to be a massive crowd on the opening day. And perhaps an unprecedented share spike that could enrich, but also go bust in a hurry. It's hard to sit this one out, but unless you're willing to stomach a big drop and double down on such a dip, it might be best to wait and see how things play out. This isn't just another tech IPO; it's the biggest one in history by one of the greatest visionaries of our time. Personally, I'd watch the rest of the Mag Seven closely and look to get in on weakness as some look to rotate capital out of the names to get ready for that SpaceX IPO launch, which could arrive as early as June 2026.

Everyone Wants to Buy the SpaceX IPO. I'm Going to Pass.

xAI is reportedly spending $1 billion a month playing catch-up as OpenAI, Anthropic, and Google continue to dominate. SpaceX recently filed for what could be the largest initial public offering (IPO) in history, targeting a massive valuation (rumored to potentially exceed $2 trillion) and a June listing. SpaceX CEO Elon Musk is reportedly structuring the offering to allocate up to 30% of the available shares for sale directly to retail investors -- three times the norm. The details behind this IPO have generated a whole lot of excitement. I get it, but I'm still going to pass on it when it finally occurs. Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue " To be sure, I think SpaceX has built something extraordinary -- perfecting reusable launch systems is truly incredible. And Starlink alone generated over $10 billion in revenue last year, helping bring the internet to underserved populations all over the globe. Image source: Getty Images. The company's $8 billion in EBITDA last year is certainly impressive. So is the $24 billion in revenue it's expected to earn in 2026. And the list of backers is a who's who of Silicon Valley: Alphabet, Sequoia Capital, and Andreessen Horowitz. Now, the obvious issue is valuation. A $2 trillion market capitalization means you would be paying more than 80 times forward revenue. That is a hefty premium, to put it lightly. But what really concerns me is the company's recent acquisition of xAI, and with it, X, the social media platform formerly known as Twitter. Neuralink and the Boring Company have been absorbed as well. The IPO bundles all of these businesses into one stock, and in my opinion, they're dead weight. X's revenue has fallen from $4.4 billion in 2022 to roughly $2.9 billion in 2025, though the steady bleed has reversed recently. The platform carries an enormous amount of debt from Musk's original $44 billion acquisition of Twitter. With $1.2 billion in annual interest payments, X is struggling to break even. Meanwhile, the latest numbers put xAI's annualized revenue at $500 million. That sounds impressive until you realize it's spending $1 billion a quarter to make that. Grok, the company's chatbot, seriously lags the offerings from OpenAI and Anthropic. All 11 of its co-founders have departed, and Musk himself said that it was "not built right." $1 billion in cash moving out the door every month is a big deal for SpaceX. Building rockets and launching satellites is an expensive business and requires a steady flow of capital. xAI will siphon off a huge portion of available funds for a return I'm not convinced will materialize. SpaceX is certainly an impressive business. But at this valuation, with xAI gobbling up cash for years to come, I'm going to pass. For me to consider jumping in, the stock would need to fall significantly. And it just might -- mega-IPOs have a history of underperforming initially. When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor's total average return is 930%* -- a market-crushing outperformance compared to 185% for the S&P 500. Johnny Rice has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Tesla. The Motley Fool has a disclosure policy.